")

Justin Sullivan

Investment thesis

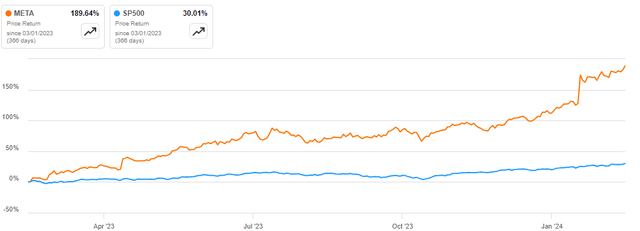

Meta Platforms, Inc. (Nasdaq: Meta) was formerly known as Facebook. Its shares have risen by about 189.64% over the past year, outperforming the Standard & Poor's 500 Index by a margin of about 160%.

Seeking alpha

With such outstanding performance, this The company presents itself as a compelling investment opportunity. Despite the stock price gains over the past year, I am bullish on this stock due to its strong financial performance, dominant market position, and strategic monetization initiatives. From a technical analysis standpoint, the company's bullish trajectory remains strong, lending more credibility to my bullish stance. The price targets for 2024 and 2025 are around $597 and $786, respectively. For these reasons, I recommend this stock to potential investors.

Price chart first

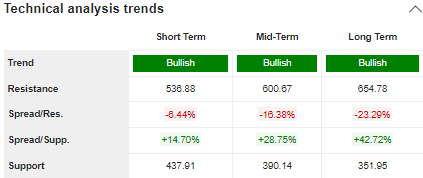

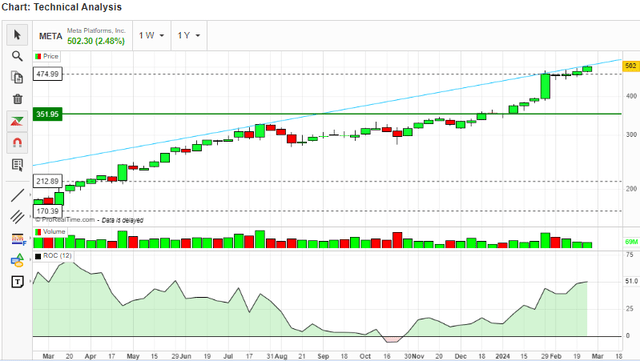

As mentioned in the previous section, META stock prices are currently experiencing upward momentum. To understand that Better yet, I will first look at the technical indicators and then I will correlate the price action to its fundamentals, especially EPS, to set my price targets. Initially, according to TradingView, META has a technical rating of 10 out of 10, which is a reflection of consistent performance in the short, medium and long term, and to confirm this assertion, all three time horizons are bullish according to TradingView.

Market examiner

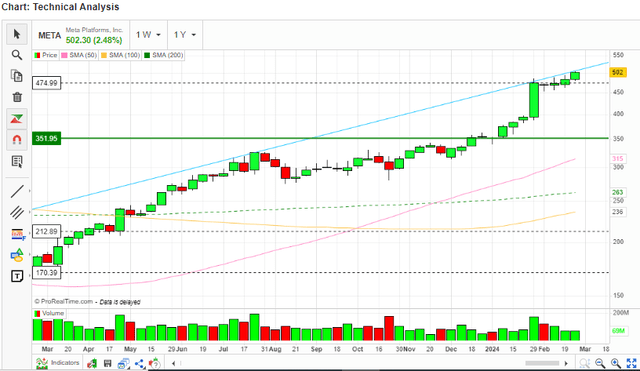

Let's dive in and evaluate what the indicators are telling us about the stock price movement. Initially, the stock price is above the 50-day, 100-day, and 200-day moving averages, which is an indication that this stock is bullish in the short, medium, and long term. More importantly, there is a bullish crossover between the 100-day moving averages and the 50-day and 200-day moving averages, indicating that the upward trajectory is very strong.

Market examiner

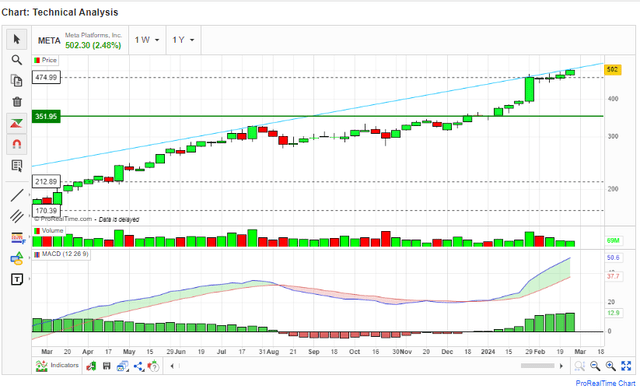

Second, the MACD is above the signal line and diverges from the signal line, which is a sign that the bullish momentum is getting stronger. This can be confirmed by the MACD histogram which is above the zero mark and growing higher with each new bar.

Market examiner

While the above indicators show that the uptrend is dominant and the bulls are in control, the most important indicator now is the rate of price change, which gives an indication of how strong the momentum is. Interestingly, the ROC is currently at 51 and growing steadily, indicating that the upward momentum is very strong and even getting stronger.

Market examiner

In short, technically, this stock currently has strong upward momentum with no signs of a reversal.

While the charts are bullish, I think it is important to correlate the price action fundamentally. In doing so, I will evaluate price changes in relation to earnings per share because the two often have a strong positive relationship. From my assessment, META's price movements were a reflection of its fundamentals and showed consistency. To support this, I will choose two scenarios. One is bearish and the other is bullish. For the bearish case, I will refer to the stock's downward movement between 2021 and 2022 as the price fell from a high of around $384 in September 2021 to a low of around $88 in October 2022, marking a stock decline of around 77%. Interestingly, between fiscal years 2021 and 2022, EPS decreased by about 37.62% from $13.77 in 2021 to $8.59 in 2022. This means that the price change was about 2.04 times the EPS change.

Now let's look at the upward price movement over the past year, during which the stock rose by approximately 189.64%. Over the last year, EPS has gained about 72.11%, rising from US$8.59 in 2022 to US$14.87 in 2023. This means that the price has changed by about 2.59 times the change in EPS.

From these two scenarios, it is clear that this stock is responding to its fundamentals, and the stock price moves about twice as much as the EPS changes. Using this background, I will develop my target price forecasts for FY24 and FY2025. To do this, I will assume that the company will achieve estimated earnings per share for the two years. Furthermore, I will assume an average EPS change of 2x to estimate price changes over the two fiscal years. With these assumptions, for fiscal year 2024, according to Seeking Alpha, the expected EPS would translate into growth of about 34.36%. Applying a 2x factor means the price will change by about 68.75%, which will translate into a target price of about $597 by the end of this year. In 2025, the estimated EPS will translate into 15.82% growth over 2024 EPS (estimated). Therefore, applying a 2x factor means that the price will change by about 31.64% from the 2024 target price, which translates to a target price of about $786 by the end of 2025.

TradingView-Author

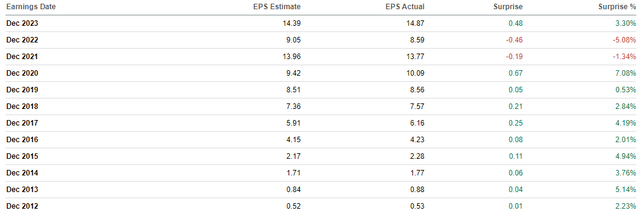

While these forecasts are based on the assumption that the company will reach its estimated EPS, it is important to evaluate how likely that assumption is. To do this, I'll draw your attention to the company's respectable history of beating estimated earnings per share. Since 2012, the company has failed to exceed estimated EPS for only two years, 2021 and 2022, largely due to the effects of the COVID-19 pandemic and inflationary economic conditions that the company appears to have overcome given its strength. Recent financial performance.

Seeking alpha

Against this backdrop, it seems very likely that this company will meet or even exceed estimated EPS targets, and therefore price targets are likely to be higher than estimated, something that would be a buffer for my rounding error, especially in the assumptions.

Strong financial performance

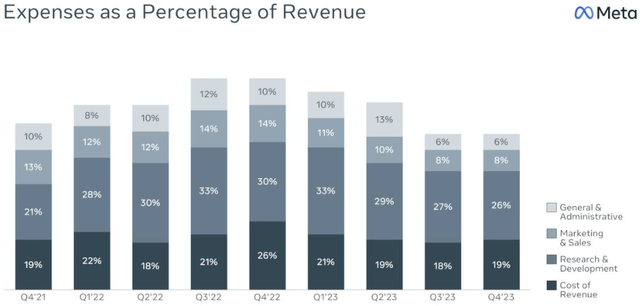

META has recently posted strong financial and health performance with a market cap of $1.28 trillion. In fiscal year 2023, revenues increased approximately 15.69% to $134.90 billion, up from $116.61 billion in 2022. In the fourth quarter of 2023 on February 1, 2024, the company reported revenues of $40.11 billion, representing growth over YoY basis is up 24.70% and beats estimates by $940.64 million. I believe these increased revenues are due to the company's growing customer base and average household revenue per person. In Q4 2023, the number of monthly active people for her family increased to 3.98 billion from 3.64 billion in Q4 2022, and her family's average revenue per person grew to $10.10 up from $7.91 in Q4 2022. In terms of profitability, the company has made great strides, with its net income growing from US$4.65 million in the fourth quarter of 2022 to US$14.02 million in the fourth quarter of 2023. These significant gains in profitability were significantly enhanced by the significant decline in Expenses as a percentage of revenue, as shown below.

Q4 Presentation

While this performance is very impressive, its sustainability and future growth are the most important aspects regarding our investments. For this reason, I will discuss why I believe this company will continue to record strong performance in the future and why it is bound to grow.

Where my future optimism stems from

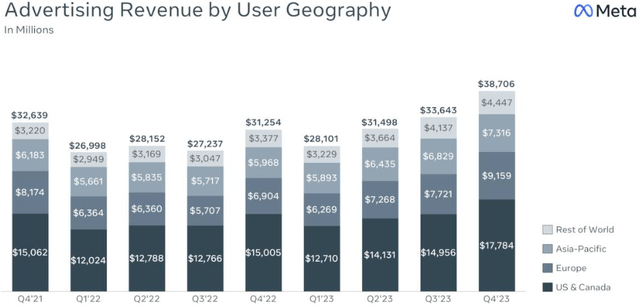

Regarding future growth and sustainability, I have several reasons for optimism. The first is the company's dominant position in the market. The company's ecosystem, which ranges from Facebook to Instagram, among other platforms, has about 4 billion monthly active users according to Statista. Importantly, these users are located in diverse geographies, which means that the company has appropriately allocated its revenue risks and is therefore virtually immune to revenue shocks if the geographic economy performs poorly. Most importantly, its broad user base provides a solid foundation for sustainable advertising revenue, which represents more than 90% of its total revenue. It is worth noting that the number of monthly active users is increasing, and this has also been reflected in advertising revenue.

Q4 Presentation

Although this company has a wide and dominant market, it has not been easy. META has demonstrated its resilience amidst headwinds, hence its sustained market dominance and performance. For example, its strategic moves to explore ad-free subscriptions and its efforts to address “shadow blocking” are a reflection of its ability to adapt to dynamic circumstances, something that instills confidence in me regarding the company's relevance and ability to survive in the wake of change. Consumer needs and regulatory environment.

Another factor that makes me believe that this company will continue to thrive in the long term is its strategic monetization strategies. Reel's products, which compete with TikTok, have reached more than 200 billion daily views across Facebook and Instagram, while monetization is rapidly growing to a more than $10 billion revenue run rate. In my view, this growth trajectory reflects strong revenue diversification potential, which is critical to the company's long-term success. The side of the reels also shows off the company's innovations, which in my opinion is a competitive advantage.

Finally, in my optimistic view, its main innovation is the Metaverse, a combination of physical and digital realities with the potential to revolutionize other sectors. According to Forbes, this innovation represents a trillion-dollar revenue opportunity. This speaks volumes about the vision and optimism in the company's revenue and overall financial health. In summary, META's future is bright supported by its dominant market position, strategic monetization and innovation.

Risks

Although I am bullish on this stock, investors need to know the risks inherent in investing here. The main risk I see here is the company's over-reliance on advertising revenue, which represents more than 90% of its revenue. This makes the Company vulnerable to fluctuations in demand for advertising, which can be affected by several factors, such as regulatory changes and changes in economic conditions. In addition, the model states that the company must maintain high user engagement, which can sometimes be a challenge. Also, the growth of the user base may reach a saturation point, which means that maintaining or sustaining its growth may be difficult at some point.

Conclusion

In conclusion, the META region is a good investment opportunity with tremendous growth potential due to its dominant market position, strong financial performance and strategic income generation supported by innovations. For these reasons, I recommend this stock to potential investors.